Imagine waking up on a Monday morning and not feeling that heavy stress in your chest. No panic about bills. No fear of “salary late ho gayi toh kya hoga.” You still work if you want to, but you don’t have to. That feeling is what most people mean when they say “financial freedom.”

Now, let’s be honest. Financial freedom is not magic. It’s not a secret app. It’s not “buy this course and become rich by Friday.” If that was true, even my neighbor’s cat would be a millionaire by now. Financial freedom is a system. A set of habits. Small steps done again and again for a long time.

In this guide, I’ll explain financial freedom kaise paaye in very simple English. I’ll talk like a real blogger who has seen real people win and lose with money. No hype. No fake promises. Just practical steps you can start today, even if you earn little.

Before we begin, let me ask you something: if your salary stopped tomorrow, how many months could you survive with your savings? One month? Two? Zero? Don’t worry if the answer isn’t great. That’s exactly why you’re here.

What is Financial Freedom Kaise Paaye? (Simple Meaning)

“Financial freedom kaise paaye” means: how to reach a stage where your basic life expenses are covered without stress, and you have enough savings and investments so you can choose your life freely.

Financial freedom does not always mean you’re a billionaire. For many people, it simply means:

You can pay rent, food, bills, and family needs comfortably

You have an emergency fund for surprises

You don’t depend on credit cards or new loans to survive

You invest regularly, and your money grows

You have multiple income sources or a strong investment income

Think of it like this. If money is a dog, you want it trained and calm. Not running around your house, breaking things, and biting your peace of mind.

Financial freedom is really about control. You control money. Money doesn’t control you.

How Does Financial Freedom Work? (Step-by-Step Explanation)

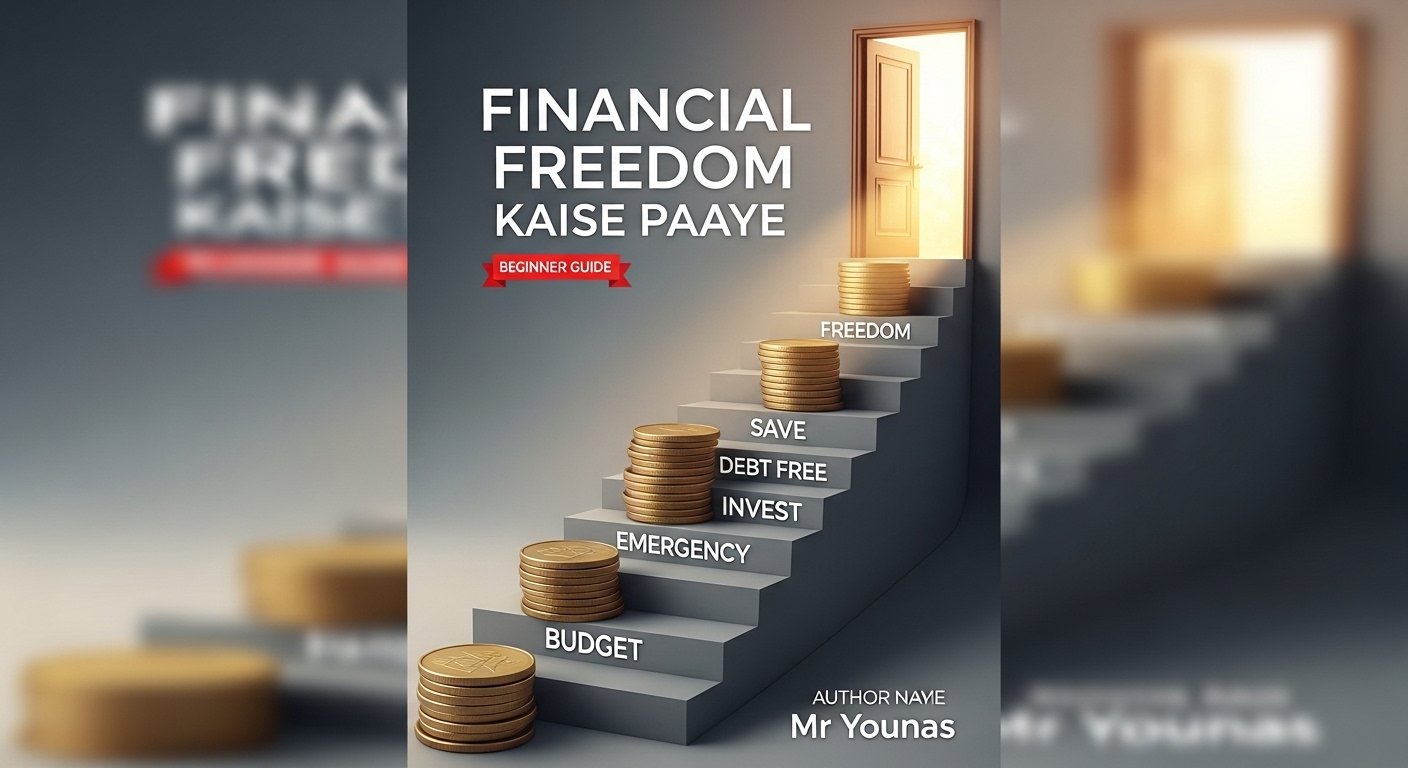

Financial freedom is not one big jump. It’s a staircase. Here’s the basic flow:

- You understand where your money goes

Most people don’t know their real spending. They guess. Financial freedom starts when you track. - You build a safety net

That’s your emergency fund so life problems don’t become money problems. - You remove high-interest debt

Debt is like a hole in your boat. You can pour as much water (income) as you want, but you won’t move forward until the hole is fixed. - You increase the gap between income and spending

That gap is your savings. Bigger gap = faster progress. - You invest the gap

Savings alone won’t beat inflation for long. Investing helps money grow. - You grow skills and income

Better income makes everything easier. It’s not always about saving more. Sometimes it’s about earning more. - You repeat for years

This is the “boring” part. And yes, boring is good in personal finance. Boring money habits often create exciting life options.

So financial freedom works like a simple engine: earn, save, invest, repeat.

Why Beginners Should Care (Even if You Earn Less)

If you’re a beginner, you might think, “I’ll focus on financial planning later. Right now I’m just surviving.” I get it. But here’s why starting early matters:

Time is your biggest advantage

If you invest early, compounding works harder. Compounding is when your money makes money, and then that money also makes money.

Small habits become big results

Saving 500 or 1000 per month feels small. But done consistently, it becomes a strong base.

Life is unpredictable

Medical expenses, job loss, family needs, sudden travel. These things happen. Financial freedom means you can handle shocks without losing sleep.

You avoid bad money traps

When you don’t have savings, you rely on loans, EMI, credit card minimum payments. Those traps keep you stuck.

Let’s do a simple example. Two friends, Sameer and Rohan:

Sameer starts investing 2000 per month at age 22

Rohan starts investing 4000 per month at age 30

Sameer invested less each month, but he started earlier. Often, Sameer can still end up with more money later because of time and compounding. It’s unfair, but it’s also beautiful if you start now.

Common Myths and Mistakes About Financial Freedom

Let’s break some myths that stop people from building wealth.

Myth 1: “Financial freedom means no work”

Reality: Many financially free people still work. They just work on their terms. They choose projects. They take breaks. They say no without fear.

Myth 2: “You need a big salary”

Reality: A big salary helps, but habits matter more. I’ve seen people earning a lot but living paycheck to paycheck because spending grows with income.

Myth 3: “Investing is gambling”

Reality: Short-term trading without knowledge can feel like gambling. But long-term investing in strong assets is not gambling. It’s planning.

Myth 4: “I’ll start after I clear all problems”

Reality: Problems never fully disappear. Start small now. Even 500 a month into a good plan can build confidence.

Myth 5: “One side hustle will make me rich overnight”

Reality: Some side hustles work well, but they take time. Anyone promising “10,000 per day guaranteed” is selling dreams, not reality.

Mistake 1: Not tracking expenses

Mistake 2: Lifestyle inflation (spending more as income increases)

Mistake 3: Keeping all money in savings account only

Mistake 4: No emergency fund

Mistake 5: Taking debt for wants, not needs

If money had a sense of humor, it would laugh the loudest when you say, “I’ll just remember my expenses in my head.” Your brain is not an accountant. It’s a storyteller.

Realistic Earning Potential (Honest Talk, No Hype)

Let’s talk honestly: how much money do you need for financial freedom?

It depends on your monthly expenses, your family responsibilities, and your lifestyle goals.

A simple approach is:

Monthly expenses x 12 = yearly expenses

Then build investments that can support a part of that yearly expense

Some people aim for investments that cover 100% of expenses. Some aim for 50% (so they can work less). Some aim for just having a big emergency fund and zero debt to feel free.

If your monthly expense is 25,000, your yearly expense is 3,00,000.

If you want investments that can support most of that in the long term, you need a serious investment base. That takes time.

But here’s the good news: financial freedom is not “all or nothing.” Even reaching the first stage, like having 6 months emergency fund and no credit card debt, feels like a huge win. It reduces stress immediately.

And yes, you can build this with a normal job. Many people do. You just need a plan and patience.

Step-by-Step Practical Guide: Financial Freedom Kaise Paaye

Now we go into the real action plan. Follow these steps in order. Don’t try to do everything in one week. Money habits are like gym workouts. You don’t get abs after one push-up.

Step 1: Know your “why” (your personal reason)

Ask yourself:

Why do I want financial freedom?

Is it to support parents? To travel? To quit a toxic job? To sleep peacefully?

Write it down in one line. Keep it on your phone notes. This “why” will help you stay consistent when motivation drops.

Step 2: Track your money for 30 days

For one month, track:

Income (salary, freelance, side income)

Fixed costs (rent, EMI, school fees)

Variable costs (food, travel, shopping)

Fun costs (movies, eating out)

Use a simple rule: don’t judge, just record. Even if you spend on something silly, write it. You’re not a bad person. You’re just collecting data.

After 30 days, you’ll see your patterns. Most people find at least 2 to 3 “money leaks” like:

Too many food delivery orders

Random online shopping

Subscriptions you forgot about

Daily auto rides instead of a cheaper option

This step alone can increase your savings.

Step 3: Create a beginner budget that doesn’t feel like punishment

Many people hate budgeting because they think it means no fun. Wrong. A good budget is permission to spend, but with limits.

Try a simple split like:

Needs: around 50 to 60%

Wants: around 20 to 30%

Savings and investing: around 10 to 20%

If your income is low, your “needs” may be higher. That’s okay. Start where you are.

Important: pay yourself first. That means saving and investing should happen soon after salary comes, not at the end of the month.

If you wait for “end of month savings,” your money will do a disappearing act. It’s like that friend who says “I’m coming” and never shows up.

Step 4: Build an emergency fund (your stress shield)

Emergency fund = money kept aside for real emergencies:

Medical issues

Job loss

Urgent family needs

Unexpected repairs

Target:

Start with 10,000 or one month expenses

Then go to 3 months expenses

Then 6 months expenses (ideal)

Keep it in a safe, liquid place where you can access fast. Don’t put emergency money into risky investments.

Emergency fund doesn’t make you rich. It makes you stable. And stability is the base of financial freedom.

Step 5: Control and clear high-interest debt

Not all debt is equal.

High-interest bad debt examples:

Credit card debt

Personal loans with high interest

Buy now pay later habit for shopping

These debts grow fast. Clearing them gives you a guaranteed “return” because you stop paying high interest.

A simple approach:

List all debts with amount, interest rate, EMI

Pay minimum on all

Put extra money toward the highest interest debt first (avalanche method)

If you need motivation, calculate how much interest you’ll pay over time. That number is painful enough to keep you focused.

Step 6: Get basic insurance (don’t skip this)

Many beginners ignore insurance because it feels like “wasting money.” But insurance is what protects your plan from one big accident.

Health insurance: very important

Term life insurance: important if you have dependents (parents, spouse, kids)

Insurance is not an investment. It’s protection. Think of it like a helmet. You don’t buy a helmet because you plan to crash. You buy it because life can be rude sometimes.

Step 7: Start investing (simple and long-term)

Once you have:

Basic emergency fund started

Debt under control (at least credit card and high interest)

A budget you can follow

Start investing.

For beginners, long-term investing is usually better than trying to “trade” daily. Trading looks exciting, but it can also empty your wallet quickly.

Common beginner-friendly options (depending on your country rules and risk profile):

Index funds

Mutual funds via SIP

Retirement accounts

High-quality diversified funds

If you don’t understand something, don’t invest in it yet. Simple wins.

A good habit: invest every month, even if the market is up or down. This builds discipline and reduces timing stress.

Step 8: Increase income (the fastest way to speed up)

Saving is powerful, but there’s a limit to how much you can cut. Income has more potential.

Beginner-friendly ways to increase income:

Upgrade skills for your job (Excel, communication, coding, design, sales)

Freelancing (writing, editing, graphic design, video editing)

Tutoring (online or offline)

Affiliate content or blogging (long-term game)

Selling a service, not just products

Pick one skill and go deep for 6 months. Don’t jump every week.

Ask yourself: what can I learn that people will pay for?

Step 9: Build multiple income streams (slowly, realistically)

Multiple income streams can be:

Active income: salary, freelancing

Semi-active: content creation, digital products

Passive-ish: investments, royalties

True passive income usually needs either:

Money upfront (investments)

Work upfront (creating content or a product)

Or both

So don’t fall for “passive income without work.” That’s like expecting six-pack abs without leaving the sofa.

Step 10: Set clear goals and track progress every month

Financial freedom is easier when it’s measurable.

Track:

Net worth (assets minus liabilities)

Savings rate (what % of income you save)

Debt reduction progress

Investment growth

Once a month, do a 30-minute money check. Make it a small routine. Tea, notebook, and calm thinking.

Tools, Platforms, and Methods That Help (Beginner-Friendly)

You don’t need fancy tools. Use what’s simple.

Expense tracking tools:

Google Sheets or Excel

Any basic budgeting app

Notes app (yes, it works)

Investment tracking:

A simple spreadsheet with SIP amount, date, and fund name

Your broker or mutual fund app portfolio view

Learning platforms:

YouTube channels (choose reliable, long-term focused creators)

Personal finance blogs (search for topics like “SIP for beginners” and “index funds explained”)

Books like: The Psychology of Money (simple lessons about behavior)

Automation methods:

Auto-debit SIP

Auto transfer to savings account

Bill reminders

Automation is powerful because it removes daily decision-making. Less willpower needed.

Tips to Succeed Faster (Without Burning Out)

- Keep lifestyle simple for a few years

You don’t need to “look rich.” You need to become stable. A fancy phone on EMI won’t impress your future self. - Increase savings rate slowly

Don’t jump from 5% to 50% and then quit. Increase by 1 to 2% whenever income increases. - Avoid comparing your journey

Someone will always earn more. Someone will always show off more. But you don’t see their debt behind the scenes. - Learn basic money skills

Budgeting, taxes, investing basics, negotiating salary. These are life skills. - Surround yourself with realistic content

If you watch too much “get rich fast” content, you’ll feel impatient and take risky decisions. - Reward yourself sometimes

A small treat keeps you consistent. Just plan it in your budget. Financial freedom should feel like a healthy lifestyle, not jail time.

Beginner-Friendly Mistakes to Avoid (Very Important)

Mistake 1: Investing without emergency fund

Then one small emergency forces you to sell investments at a bad time.

Mistake 2: Chasing hot tips

“Buy this stock, it will double.” Most tips are noise. Build a plan, not a rumor collection.

Mistake 3: Overusing credit cards

Credit cards are useful if you pay full bill on time. If you pay minimum due, it becomes very costly.

Mistake 4: Not improving income skills

If you only focus on cutting expenses, growth becomes slow. Skills increase your earning power.

Mistake 5: Ignoring health

Medical bills can destroy savings. Also, if you’re not healthy, even money won’t feel like freedom.

Mistake 6: Buying things to impress people

This is a classic trap. People forget your new shoes in 2 days. But you’ll remember the EMI for 12 months.

Mistake 7: Stopping investments when market is down

Market down is scary, but long-term investors often benefit from continuing SIPs in bad times.

FAQs (Financial Freedom Kaise Paaye)

1) Financial freedom kaise paaye if my salary is low?

Start with basics: track expenses, cut money leaks, build a small emergency fund, and start a small SIP or index fund investment. Also focus on skill building to increase income. Even 500 or 1000 per month invested consistently is a strong start.

2) How much money do I need to become financially free?

It depends on your monthly expenses and lifestyle. A simple way is to calculate your yearly expenses and then build investments over time that can support those expenses. You can also aim for partial freedom first, like having 6 months expenses saved and zero high-interest debt.

3) Is SIP enough for financial freedom?

SIP is a method, not a magic product. SIP in good funds can help you build wealth long-term, but you also need budgeting, emergency fund, insurance, and income growth. SIP works best when you stay consistent for years.

4) Should beginners invest in stock market directly?

If you’re a beginner, it’s safer to start with diversified options like index funds or mutual funds, and learn slowly. Direct stocks need time, knowledge, and emotional control. First build a base, then explore.

5) What is the biggest mistake that stops financial freedom?

Living without a plan. No budget, no emergency fund, and taking high-interest debt for wants. These three things keep people trapped even with a decent income.

6) How long does it take to achieve financial freedom?

It usually takes years, not months. The timeline depends on income, savings rate, investment returns, and life responsibilities. But the good part is you start feeling better much earlier as soon as you build an emergency fund and control debt.

7) Can I achieve financial freedom without taking risks?

Some risk is part of growth because inflation reduces money value over time. But you can manage risk by investing long-term, diversifying, and avoiding shady schemes. The goal is smart risk, not wild risk.

Final Conclusion (Motivation Without Fake Hype)

Financial freedom kaise paaye is not about becoming “rich” in a dramatic way. It’s about becoming strong and calm with money. It’s about sleeping better, handling emergencies, and making life choices without fear.

Start with one step today. Track your expenses. Build a small emergency fund. Stop one unnecessary subscription. Begin a tiny monthly investment. Learn one skill that increases your income.

You don’t need perfect conditions. You need a simple plan and consistency.

And whenever you feel slow, remember this: money growth is like growing a tree. You water it, you protect it, you wait. One day, you’ll sit under its shade and think, “Good thing I started.”

If you want, tell me your age, monthly income range, and monthly expenses range, and I’ll suggest a simple beginner plan (budget split + emergency fund target + starting investment approach) in the same easy style.